Introduction

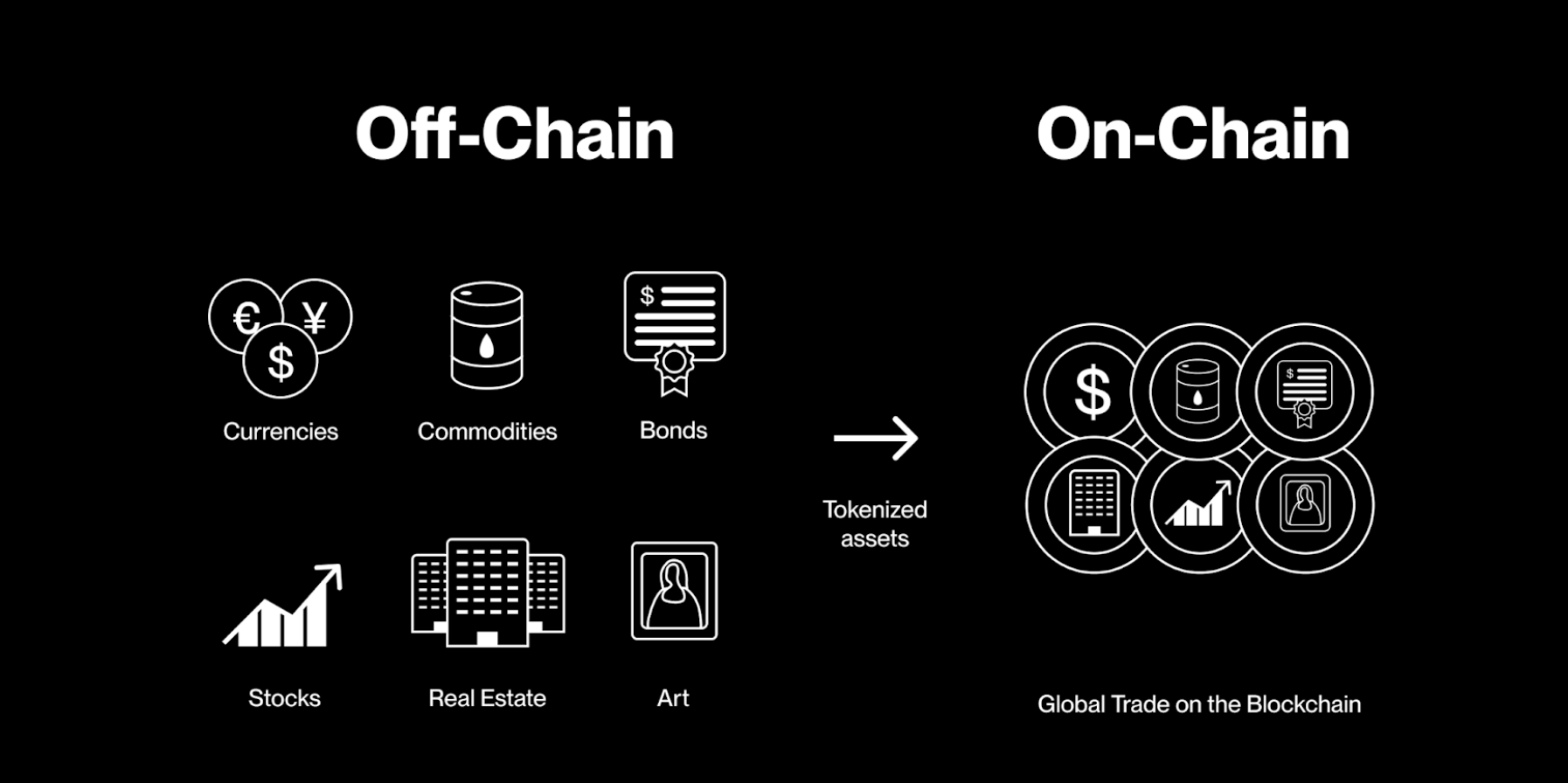

Asset tokenization is a transformative process that leverages blockchain technology to represent real-world assets (RWAs) as digital tokens. According to the Financial Stability Board (FSB, 2023), tokenization refers to the process of representing an asset as a digital record on a common programmable platform using distributed ledger technology (DLT).

This method, a modern evolution of traditional securitization, digitizes ownership rights, enabling fractionalization, enhanced liquidity, and streamlined transactions.

By converting assets like real estate, art, or financial instruments into programmable digital tokens, tokenization is poised to reshape global financial markets. This report provides an overview of the current state of asset tokenization, examining its market dynamics, key drivers, regulatory landscape, and future trajectory.

The Current Market Landscape

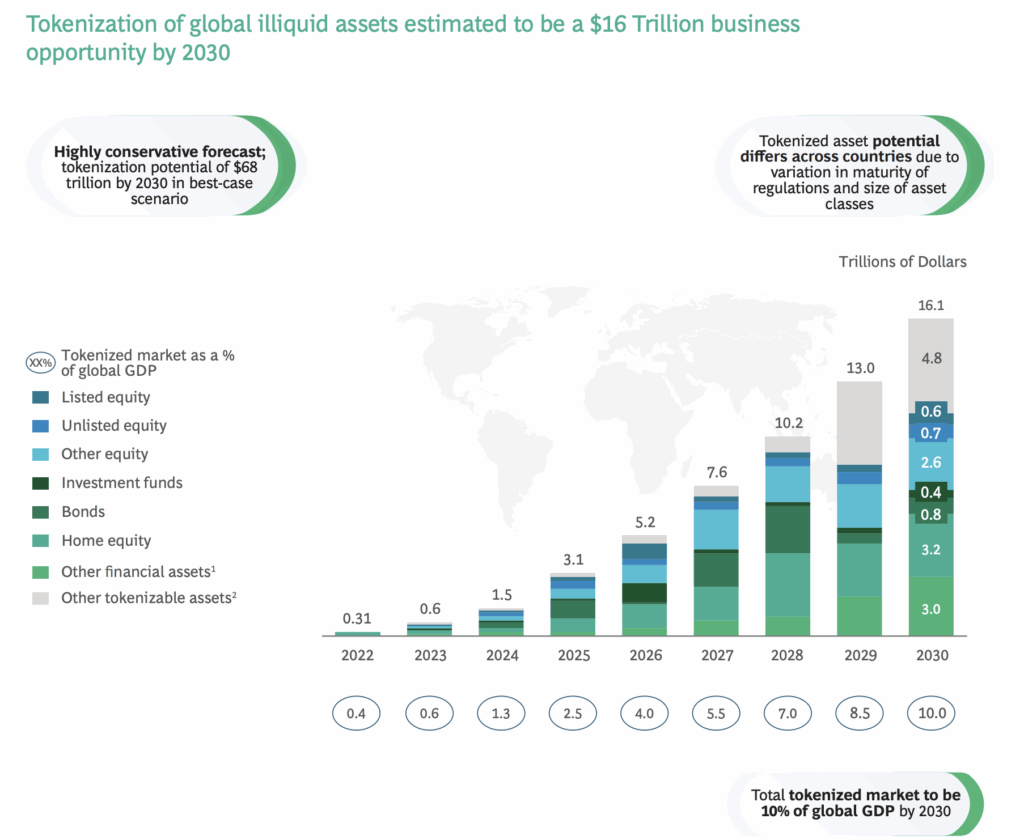

The market for asset tokenization is experiencing a period of rapid growth and institutional acceptance. While still considered a nascent market by some, with a value of approximately $30 billion, its potential is immense. According to a joint study by BCG and ADDX, the value of tokenized assets is projected to reach an impressive $16.1 trillion, or 10% of global GDP by 2030. This growth is driven by a confluence of factors, including increasing digitalization and a growing appetite from both institutional and retail investors for more accessible investment opportunities. Market projections vary, with some estimates suggesting a compound annual growth rate (CAGR) of over 75% across various asset classes, a rate significantly faster than traditional financial markets.

Geographically, North America currently holds the largest market share. However, regions like Asia-Pacific and the Middle East are emerging as fast-growing hubs, driven by rapid digitalization and government-backed initiatives like Singapore’s Project Guardian. A key trend in the current market is the significant involvement of major financial institutions such as BlackRock, Goldman Sachs, and JPMorgan, which are actively exploring and launching tokenized funds and financial products. This institutional adoption is a critical validator for the technology, fostering market confidence and driving mainstream integration.

The Asset Tokenization Process

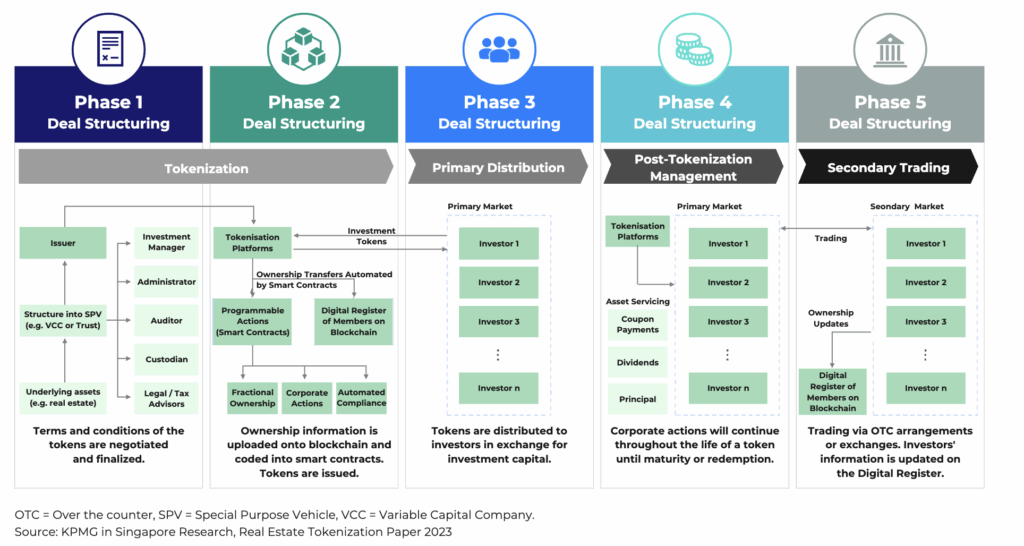

The process of tokenizing an asset requires careful legal, technical, and regulatory consideration. The general framework involves these key stages:

- Legal Structuring: A legal entity, often a Special Purpose Vehicle (SPV), is created to hold the asset, and a legal framework defines the rights associated with the tokens.

- Asset Valuation: The asset undergoes a professional appraisal to determine its fair market value.

- Smart Contract Development: A smart contract is built on a chosen blockchain to govern the token’s rules, including issuance and transfer.

- Token Issuance and Onboarding: Digital tokens are minted, and they are issued to investors after mandatory KYC and AML checks.

- Trading and Management: Tokens are distributed to investors and listed on secondary markets to provide liquidity, with ongoing management handling tasks like dividend payments and compliance.

Key Drivers and Tokenized Assets

The core appeal of asset tokenization lies in its ability to solve long-standing problems in traditional finance. The primary drivers of its adoption include:

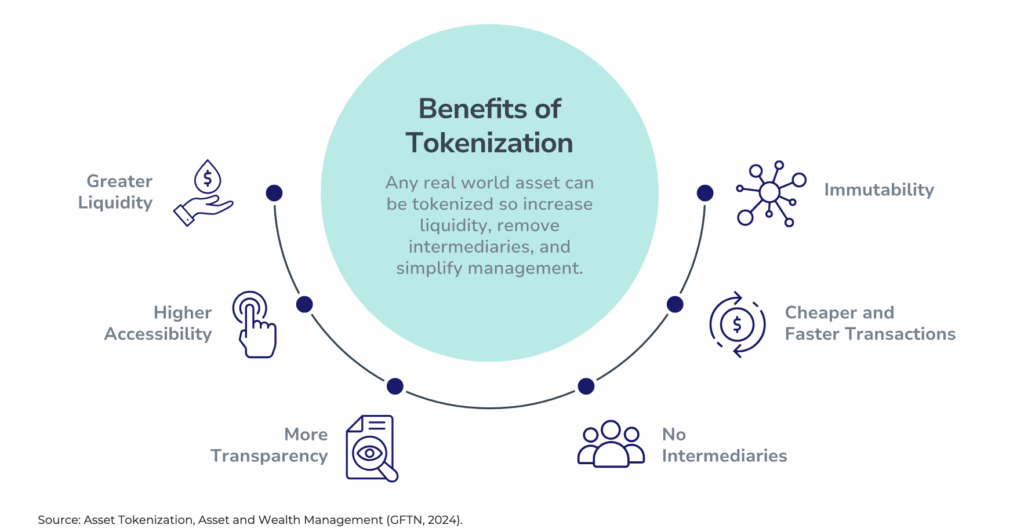

- Fractional Ownership: Tokenization allows high-value, illiquid assets to be divided into smaller, more affordable units. This democratizes investment by lowering the barrier to entry for retail investors who can now own a fraction of a commercial property, a piece of fine art, or a private equity fund.

- Increased Liquidity: By creating digital tokens that can be traded on secondary markets 24/7, tokenization introduces liquidity to historically illiquid assets. This gives investors greater flexibility to buy and sell their holdings without lengthy and cumbersome traditional processes.

- Enhanced Transparency and Efficiency: Transactions are automated by smart contracts on a blockchain, which creates an immutable and transparent record of ownership and transfers. This reduces the need for intermediaries, cuts down on administrative costs, and significantly accelerates settlement times, which can be near-instantaneous. The ability for a platform to allow for pre-determined conditions to be encoded with the tokenized assets can also facilitate greater straight-through processing.

- Programmability and Composability: Tokenization allows for programmability, which means certain functions of an asset’s life cycle can be automated and extended through smart contracts. This leads to “composability,” a concept akin to Lego bricks, where different tokenized assets and financial protocols can be combined to create innovative financial products and services. This enables new use cases like atomic trading, settlement, and custody all happening at the same time, eliminating settlement risk.

A wide variety of assets are currently being tokenized, with real estate and financial instruments leading the way. The primary asset classes include:

- Real Estate: High-value properties are a prime candidate for tokenization due to their high entry cost and illiquidity. Platforms are allowing investors to purchase fractional shares of properties and receive proportional rental income. The real estate tokenization market is anticipated to exceed $16.5 billion by 2033.

- Financial Instruments: This is a major area of focus for institutional players. Examples include the tokenization of private credit, government treasury bonds, and money market funds. The notional value of tokenized bonds issued globally totals over $10 billion, and tokenized money market funds have attracted over $1 billion in assets under management.

- Art and Collectibles: Tokenization is disrupting the traditional art market by enabling fractional ownership of valuable artworks, making this asset class accessible to a broader audience. Examples include the tokenization of a piece by Pablo Picasso.

- Commodities: Gold and other precious metals are also being tokenized, with tokens backed by physical reserves, providing a new way for investors to hedge against market volatility. The global market for this is projected to reach $13.2 billion by 2032.

- Intangible Assets: Tokenization is expanding into new areas like intellectual property, movies, and songs. For example, a collaboration between IBM and IPwe tokenized 25 million patents into NFTs. In Thailand, regulations have been introduced for green tokens and the tokenization of movies and songs.

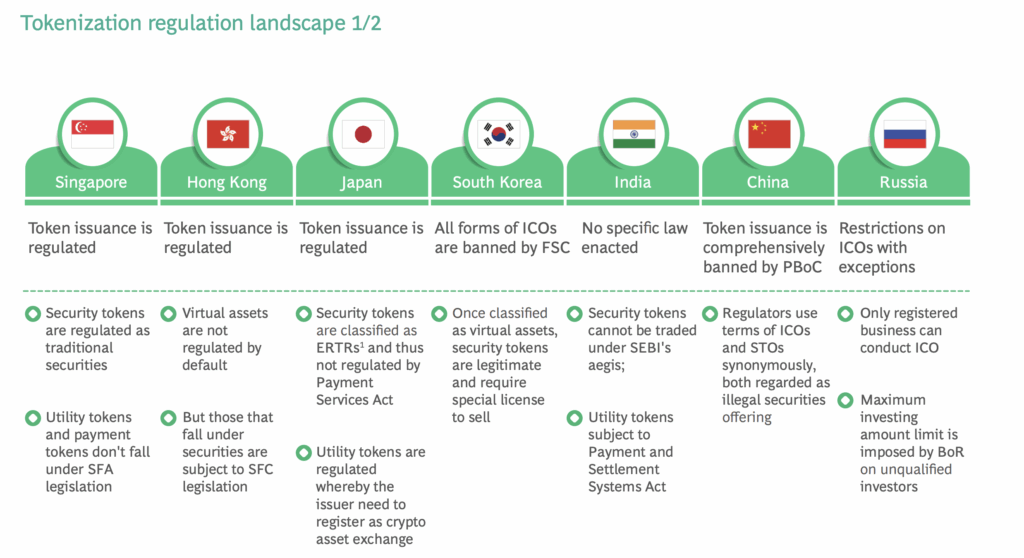

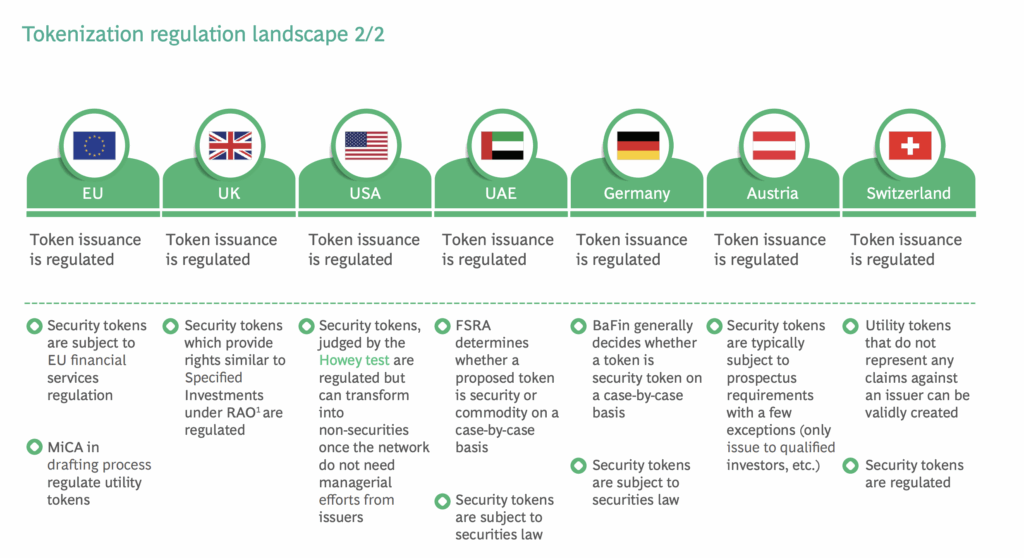

Regulatory and Legal Considerations

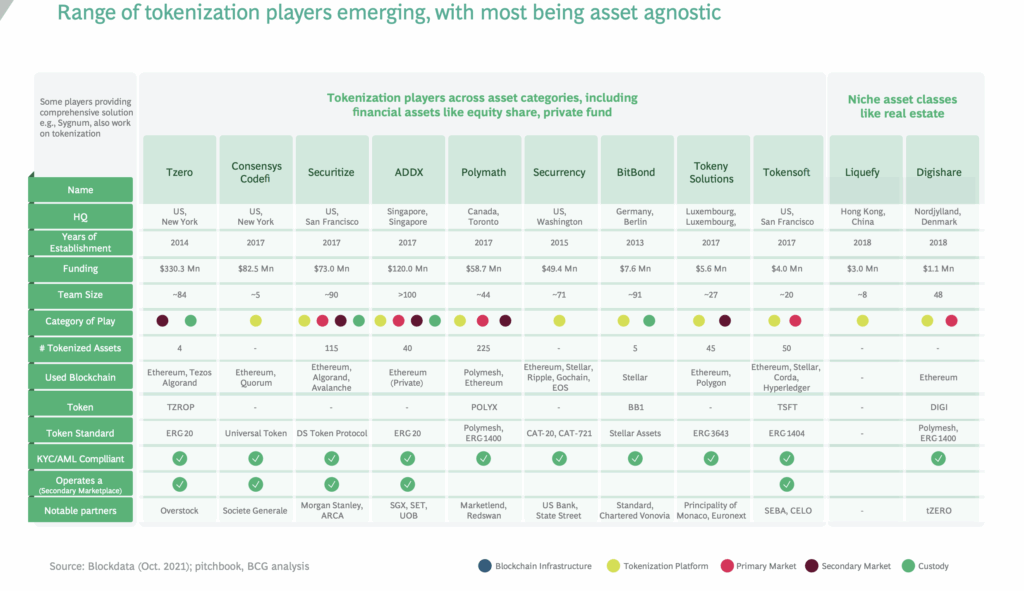

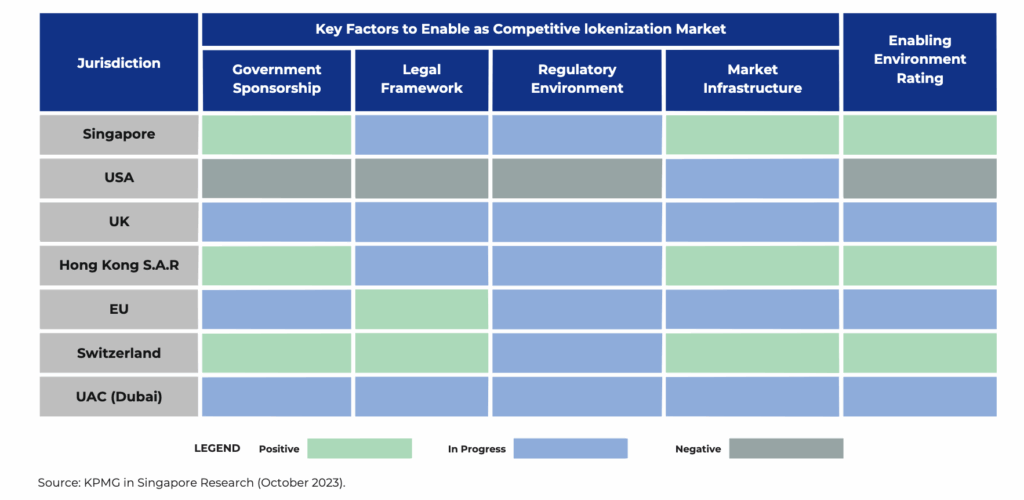

The regulatory landscape for asset tokenization is still in its nascent stages and is characterized by fragmentation and uncertainty. A major challenge is the lack of a universally accepted classification for tokens. Regulators in different jurisdictions are grappling with whether tokens should be classified as securities, utility tokens, or a new asset class, which dictates the legal and compliance requirements for issuance and trading. Initiatives like Singapore’s Project Guardian are instrumental in showcasing successful pilot programs and are helping to inform a collaborative approach with the industry to solve problems of scale.

Key regulatory hurdles that companies must navigate include:

- Token Classification: The U.S. Securities and Exchange Commission (SEC) often classifies tokens representing ownership as securities, subjecting them to stringent registration and disclosure laws. Other jurisdictions, like Switzerland and Singapore, have established more progressive regulatory frameworks, attracting tokenization initiatives.

- Compliance with KYC and AML: To prevent fraud and illicit activities, platforms must implement robust Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures.

- Cross-Border Complexity: The global nature of blockchain means that tokenization platforms must comply with varying laws and regulations across different countries, adding a layer of legal complexity.

Leave a Reply