Central Banks Deepen CBDC Exploration

Central banks around the world continued to make significant progress in their exploration of central bank digital currencies (CBDCs) in 2024, according to the latest report from the Bank for International Settlements (BIS). Out of 93 central banks surveyed, 91% were engaged in some form of CBDC work, whether retail, wholesale, or both. While this represents a slight dip from 2023’s 94%, the overall momentum remains strong—especially as wholesale CBDCs move into more advanced stages than retail initiatives.

Wholesale CBDCs Lead the Way

The BIS survey highlights that wholesale CBDCs (wCBDCs)—digital currencies designed for interbank and institutional use—are progressing faster than their retail counterparts.

- In advanced economies (AEs), 38% of central banks are running wholesale pilots and 17% are developing live systems. By contrast, retail CBDC pilots remain limited, with 15% in pilot phase and none live.

- In emerging market and developing economies (EMDEs), 35% are experimenting with wholesale CBDCs compared with 27% experimenting with retail. Additionally, 16% of EMDEs are piloting wholesale CBDCs.

This contrasts with the retail space, where only three central banks—The Bahamas, Jamaica, and Nigeria—have launched live retail CBDCs. While no new retail projects went live in 2024, 48% of central banks are running experiments and 19% are piloting projects, signaling a growing pipeline.

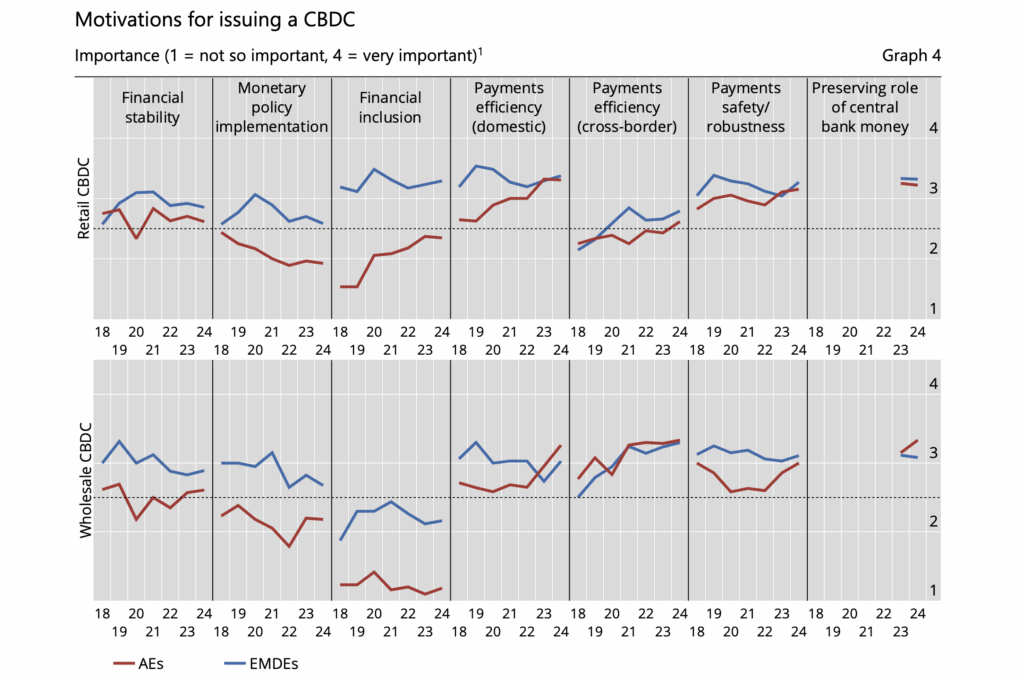

Why CBDCs? Preserving the Role of Money

A central motivation behind CBDC exploration is preserving the role of central bank money in an increasingly digital economy.

- Nearly 80% of central banks working on retail CBDCs and 75% on wholesale CBDCs see this as an important reason for issuance.

- The decline of cash is driving retail CBDC work, as many central banks view sovereign digital alternatives as essential for maintaining trust in money.

- Wholesale CBDCs, meanwhile, are seen as crucial to ensuring central bank money continues to function as a settlement asset in tokenised financial markets.

For retail CBDCs, other top drivers include domestic payment efficiency, safety, and in EMDEs, financial inclusion. Wholesale CBDC work, by contrast, is primarily driven by enhancing cross-border payments—a long-standing pain point in global finance.

Use Cases: Everyday Payments vs Market Infrastructure

The envisioned applications differ sharply between retail and wholesale CBDCs:

- Retail CBDCs: Focused on everyday use—peer-to-peer payments (81%), point-of-sale transactions (79%), and government payments (76%).

- Wholesale CBDCs: Target financial infrastructure—interbank settlements (84%), delivery versus payment for securities (77%), and payment versus payment for FX (70%).

Some wholesale designs also anticipate more advanced use cases, such as automated margin calls and settlement of tokenised deposits.

Distribution, Access, and Adoption Models

How CBDCs are delivered to end users is another key focus area:

- Over two-thirds of central banks expect retail CBDCs to be distributed through commercial banks.

- Around half also plan to involve non-bank payment providers, increasing reach and competition.

- To ensure adoption, 33% of AEs and 58% of EMDEs may require merchants to accept CBDC.

- Access is also being debated: while 40% of central banks are considering wallet-based access without a bank account, others may require accounts—particularly in EMDEs (19%).

The digital euro, for example, would be distributed via commercial banks and post offices, ensuring broad accessibility.

Fees, Limits, and Remuneration

Central banks are carefully balancing incentives and safeguards in CBDC design:

- 50% of AEs plan to make basic CBDC services free, as with the proposed digital euro.

- Most central banks do not intend to pay interest on retail CBDCs.

- Many are considering holding and transaction limits to prevent destabilising bank outflows—an approach already floated by the European Central Bank.

Advanced Features: Interoperability, Offline Use, and Programmability

CBDC design is moving beyond payments into infrastructure innovation:

- Interoperability is a priority, with 56% of AEs and 79% of EMDEs exploring integration with domestic systems, and many also considering cross-border interoperability.

- Offline functionality is under active study, including pilots in Hong Kong (e-HKD) and India (digital rupee).

- Programmability—automating payments or embedding rules—features in both retail and wholesale CBDC planning. Interestingly, EMDEs are more likely than AEs to consider programmable retail CBDCs, while AEs lead in programmable wholesale designs.

- Use of distributed ledger technology (DLT) remains divided: only 6% of AEs envision DLT-based retail CBDCs, compared to 40% of EMDEs.

Looking Ahead

The BIS report underscores a clear global trend: CBDCs are moving from theory to practice. Wholesale projects are further along, driven by cross-border and institutional use cases, while retail CBDCs remain experimental but increasingly viewed as essential to the future of money.

The diversity of approaches—whether in distribution models, limits, programmability, or technology choices—reflects the unique economic, financial, and political contexts in which central banks operate.

Leave a Reply