The financial world is undergoing a digital revolution. At the center of this transformation are two approaches to representing fiat currency on blockchain networks: stablecoins and tokenized deposits. Both promise faster, programmable, and more efficient financial transactions—but they differ fundamentally in structure, purpose, and regulatory treatment.

Understanding these differences is essential for banks, fintechs, regulators, and anyone navigating the future of money.

The Contenders: Two Visions for Digital Money

Stablecoins: The Disruptors

Stablecoins are digital assets issued primarily by private, non-bank entities such as Tether (USDT), Circle (USDC), and PayPal’s PYUSD. They are pegged 1:1 to fiat currency and backed by reserves—typically a mix of cash, custodial accounts, and short-term government securities.

Their appeal lies in accessibility. Anyone with an internet connection and a digital wallet can use stablecoins, bypassing traditional banking intermediaries. Operating on public blockchains, they enable 24/7 global transactions that settle in seconds at minimal cost.

However, this openness comes with trade-offs. Stablecoins:

- Lack FDIC insurance and other bank protections ( USDC benefited from FDIC insurance after SBV failure). Stablecoins like USDC generally lack FDIC insurance or traditional bank protections. Normally, FDIC coverage is capped at $250,000 per depositor, but during the SVB collapse regulators took extraordinary measures by guaranteeing all deposits, far beyond the usual limit. This wasn’t aimed at protecting stablecoins, yet Circle—and by extension USDC holders—benefited indirectly from the intervention.

- Have proven vulnerable, as seen with TerraUSD’s collapse (2022) and USDC’s temporary depeg (2023 banking crisis).

Despite these risks, stablecoins have become essential infrastructure in crypto markets, cross-border payments, and DeFi ecosystems.

Tokenized Deposits: The Evolutionaries

Tokenized deposits are banks’ answer to digital transformation. They are digital representations of existing bank deposits, minted on a blockchain and fully backed by funds that remain on the bank’s balance sheet. Examples include JPMorgan’s JPM Coin.

Unlike stablecoins, tokenized deposits:

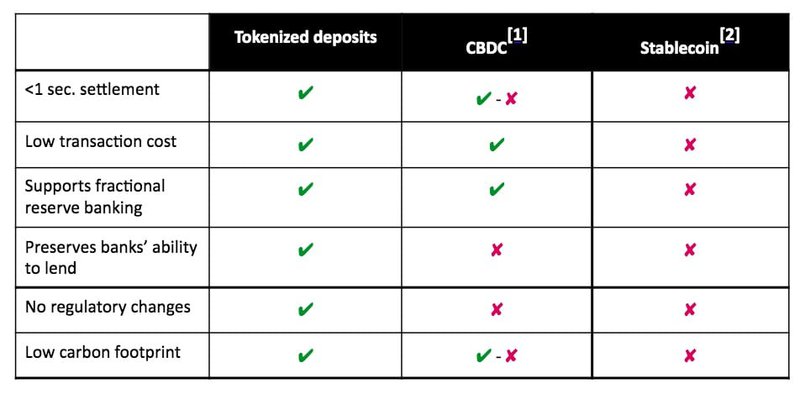

- Remain within regulated banking frameworks, benefiting from Basel III standards and FDIC insurance.

- Operate on permissioned blockchains, prioritizing security, compliance, and institutional use.

- Support liquidity and credit creation, since deposits stay within the banking system rather than being moved to custodial reserves.

- Positive impact (real time liquidity) on liquidity : Tokenized deposits enable instant interbank payments without reliance on traditional settlement systems such as ACH or wire transfers. For example, Citi has demonstrated how tokenized deposits can facilitate real-time cross-border liquidity transfers between branches, enabling large-value payments to settle continuously, regardless of time zones or central bank hours. This significantly improves liquidity management and reduces delays in time-sensitive financial operations.

- Reduced counterparty risk – By minimizing reliance on traditional payment rails, tokenized deposits mitigate counterparty and settlement risks.

- Enhanced security and transparency – Built on secure, permissioned DLT infrastructure, tokenized deposits provide improved auditability and regulatory compliance while ensuring privacy and control.

- Greater security and trust – Improved transparency helps protect customers from fraud and financial crime, ensuring safer and more reliable transactions.

Tokenized deposits could bring major improvements to the repo market by allowing banks to bypass traditional payment rails, delay settlement, and execute atomic transactions on their own schedules. In today’s repo market, each transaction must settle before the next can occur, which ties up liquidity until payments clear. With tokenized deposits, banks can postpone final settlement, freeing liquidity and enabling more flexible intraday repo activity. This flexibility supports both internal and client trades, while reconciliation over legacy rails can be consolidated into a single end-of-day transaction—reducing counterparty and settlement risk, and potentially lowering costs.

Furthermore, active management of intraday liquidity is poised to unlock up to $150mn in annual cost savings for every $100bn in deposits (src R3).

Their strength lies in institutional applications such as real-time corporate settlements, treasury automation, and cross-border interbank transactions.

Key Differences: Beyond the Surface

| Feature | Stablecoins | Tokenized Deposits |

|---|---|---|

| Issuer | Non-bank entities (e.g., Circle, Tether, PayPal) | Regulated banks (e.g., JPMorgan) |

| Backing | Off-balance-sheet reserves (cash, Treasuries) | On-balance-sheet deposits |

| Insurance | Not FDIC-insured | FDIC-insured (where applicable) |

| Blockchain | Public, open-access | Permissioned, controlled |

| Liquidity Impact | Remove liquidity from banking system | Keep liquidity within banks |

| Use Cases | Retail payments, DeFi, remittances | Institutional settlement, B2B, treasury ops |

Points of Convergence: Where They Align

Despite their differences, stablecoins and tokenized deposits share common ground:

- Programmability: Both can be embedded into smart contracts and enable automated, conditional payments.

- Speed: Transactions settle in near real-time, avoiding legacy settlement delays (ACH, SWIFT).

- Modernization: Both move financial infrastructure toward programmable, 24/7 money rails.

At their core, both are blockchain-based representations of fiat currency designed to make payments faster, cheaper, and more flexible.

Economic and Regulatory Implications

- Stablecoins may weaken bank balance sheets over time, since reserves are often parked in safe assets outside the banking system, reducing banks’ ability to lend.

- Tokenized deposits preserve banks’ role in credit creation, ensuring liquidity stays within the financial system.

On the regulatory front:

- Stablecoins face uncertain frameworks. Proposals like the U.S. GENIUS Act would impose strict requirements on issuers. The EU’s MiCA is pushing toward harmonized regulation.

- Tokenized deposits fall under existing banking law, easing regulatory hurdles.

The Road Ahead: Coexistence or Convergence?

The future is unlikely to crown a single winner. Instead, stablecoins and tokenized deposits will likely coexist, serving different niches:

- Stablecoins will dominate retail-facing and crypto-native applications, thanks to their borderless accessibility and integration with DeFi.

- Tokenized deposits will transform institutional finance, powering interbank settlements, corporate payments, and integration with wholesale CBDCs.

Initiatives like the BIS’s Project Agorá aim to unify ledgers for tokenized deposits and CBDCs, hinting at a hybrid model that blends the safety of traditional finance with the speed and innovation of decentralized infrastructure.

Final Takeaway

Stablecoins and tokenized deposits are not rivals so much as complements in the evolution of programmable money. Stablecoins bring speed, accessibility, and global reach; tokenized deposits bring safety, compliance, and integration with the existing banking system.

Together, they represent the next stage in financial infrastructure—a shift away from slow, batch-based systems toward real-time, programmable, and interoperable money.

Leave a Reply